|

Getting your Trinity Audio player ready...

|

News publishers, still coming to grips with the switch to digital and a loss of print advertising revenue, are exploring new business models to offset a global loss of £28bn in revenue over the past 5 years, according to a new WARC report.

At the same time, digital’s share of publishers’ ad income is growing, total online content consumption is increasing, consumers are fine with ad-supported business models, global ad spend is set to rise 5% this year, and online video is on track to record its strongest growth ever.

These and other key findings are included in the latest report focusing on print and digital publishing compiled by WARC, the international authority on advertising and media effectiveness.

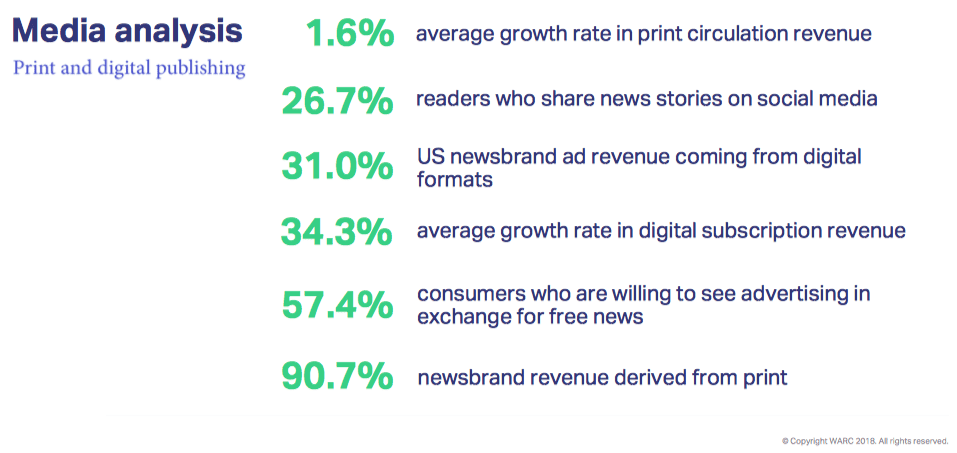

Interestingly, print (advertising and circulation) still accounts for over 90% of newsbrands’ revenue worldwide, though the majority now comes from circulation.

According to the report, print circulation revenue has grown by around 1.6% each year, rising from $80.4bn in 2012 to an estimated $86.8bn in 2017 – 57.5% of the total. Digital subscription revenues are also up year-on-year, though at an estimated $3.9bn in 2017, they still only account for 2.6% of total earnings.

What’s next? Diversification

The WARC Publishing Report states that most publishers believe their business will diversify to offset the downturn. A survey of 250 news industry decision makers found that many believe their business models will need to radically change if they are to meet future expectations.

Here are some of the projections and pointers from the WARC report:

- Most (25%) respondents believe that non-traditional revenue sources (i.e. those beyond circulation, subscriptions, and advertising) account for less than 10% of total income. By 2022, most (21%) believe non-traditional income will contribute between 31% and 40% towards the bottom line.

- Salon, one of the first online-only magazines, recently gave users the option to donate unused computing power to mine cryptocurrency as an alternative to seeing advertising messages.

- Legislation may also provide publishers with a new revenue stream. The EU is considering introducing a new law (Article 11) which would require online properties – including Google and Facebook – to pay licensing fees to publishers for hosting snippets of and providing links to third-party content. Opponents have dubbed this the “link tax”, though publishers argue the proposal safeguards copyrighted material from content aggregators.

In the UK, several newsbrands have recently come together to enable advertisers and agencies to buy digital inventory across their titles and access a combined audience roughly on a par with Facebook’s reach in the country – which could indicate possible future models for other publishers.

Ads are OK, say consumers

Fortunately for publishers, the report indicates that ad-supported business models are still palatable for consumers.

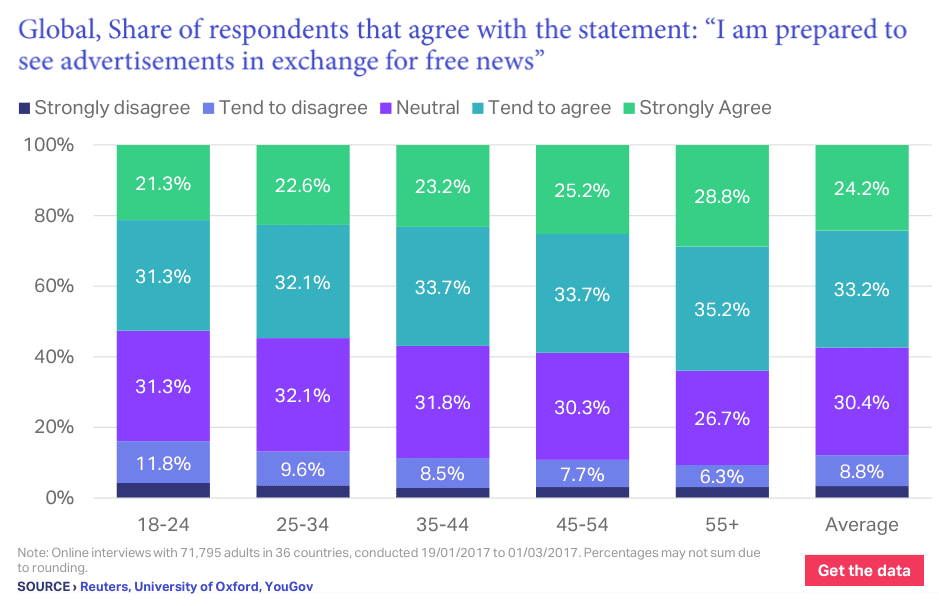

The majority of consumers are still willing to view advertising in exchange for free news, a survey by Reuters has confirmed. A full 57.4% on average agree, with 24.2% strongly agreeing.

Which is good news, as the latest WARC research on the state of the global ad market finds:

- Budget growth is positive across all regions

- Digital budgets continue to expand rapidly

- Global ad spend to rise 5% this year

- Online video set to record the strongest growth this year

WARC predicts that online video is expected to be the fastest-growing ad medium this year, with spend rising by approximately 29.7% on a PPP basis, according to data included in WARC’s latest International Ad Forecast.

Much of the online video growth will come from increased spend on mobile, which is also anticipated to record rapid growth (+26.3%) this year.

“The data underline the scale of the challenge facing publishers – despite robust consumer interest in their products,” says James McDonald, WARC’s Data Editor.

The response appears to be to club together to build scale, to emphasize the importance of context and brand safety, and to diversify revenue streams, particularly into native and branded content.

While things are definitely changing across the board, and in a more accelerated fashion than ever before, there’s a lot of good news too. And more publishers are willing to adapt and make the changes necessary, to thrive in this increasingly digital age.