|

Getting your Trinity Audio player ready...

|

For many publishers, a key priority for the year ahead involves growing revenues from readers. This is nothing new. In recent years, the rise of paywalls and move to subscriptions has been a major trend across the media landscape.

However, despite this focus, publishers need to ask tough questions about the potential – and sustainability – of this income stream. So, what do we know about the subscription landscape, and what questions should publishers be asking themselves?

In this two part series, we look at the lie of the land and determine the most important strategic questions that publishers – large and small – need to address.

To kick things off, here are five major subscription trends to note:

1: Growing subscription revenues is a priority

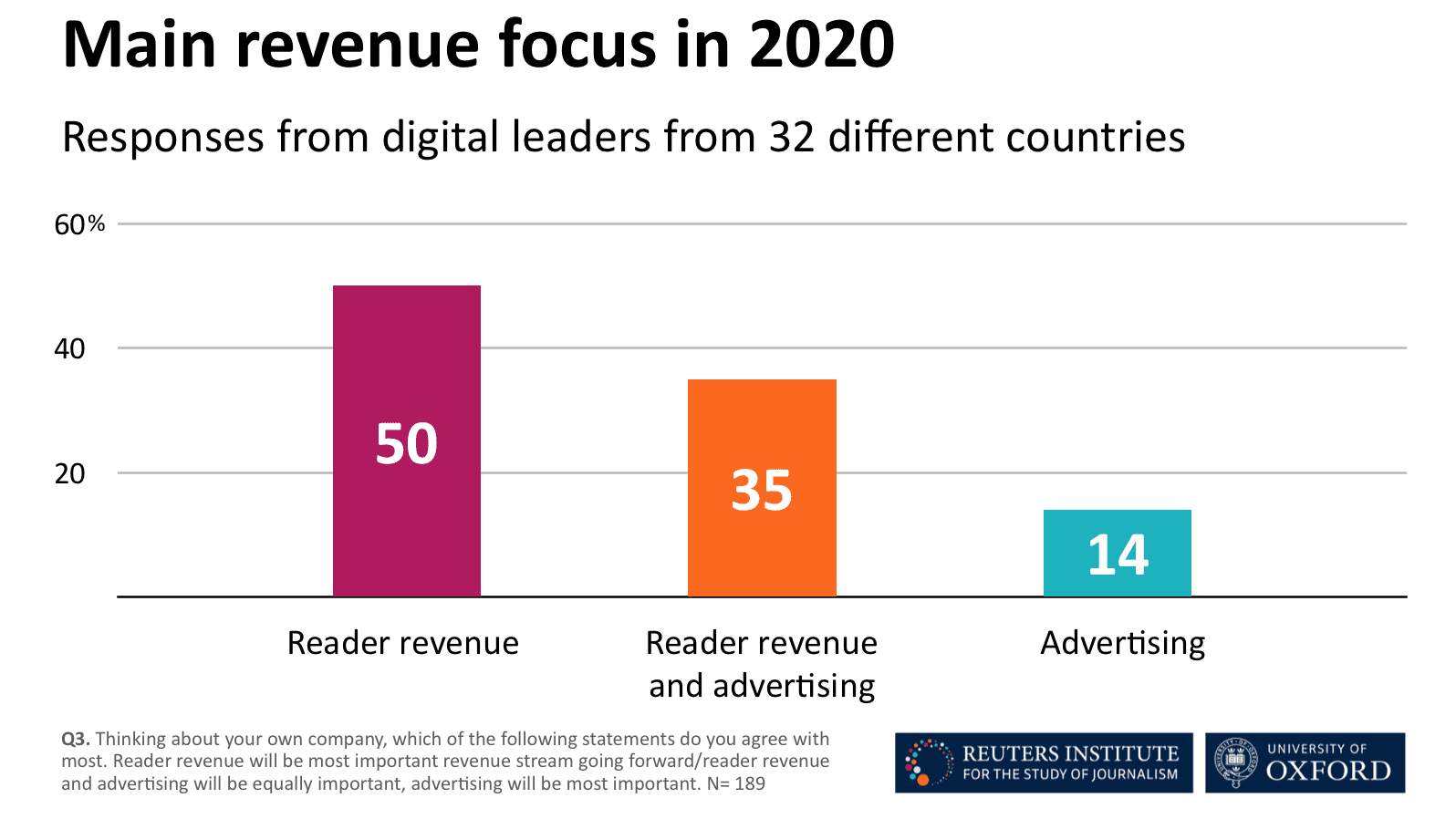

According to Journalism, Media, and Technology Trends and Predictions 2020, an annual report published by the Reuters Institute for the Study of Journalism (RISJ), half (50%) of the digital leaders indicated that subscriptions will be their main revenue focus.

The findings, from a survey of senior executives in 32 different markets, mirrored similar conclusions from a study produced by Digiday. Of the 135 publishers (location/markets not given) surveyed by Digiday “In 2020, the biggest focus for all publishers was on growing subscription revenue and revenue from direct-sold advertising.”

One key reason for this emphasis, notes Nic Newman, author of the Reuters’ predictions study, is that:

“News executives across many countries tell us that reader revenue is providing stable and growing income while advertising has remained volatile, with many reporting worse than expected results in 2019.”

As a result, based on RISJ’s global sample, just over a third (35%) saw advertising and reader revenue as equally important.

Just one in seven (14%) felt that advertising would, or should be, their primary focal point for revenue in the year ahead.

2: NYT and WSJ are leading the pack

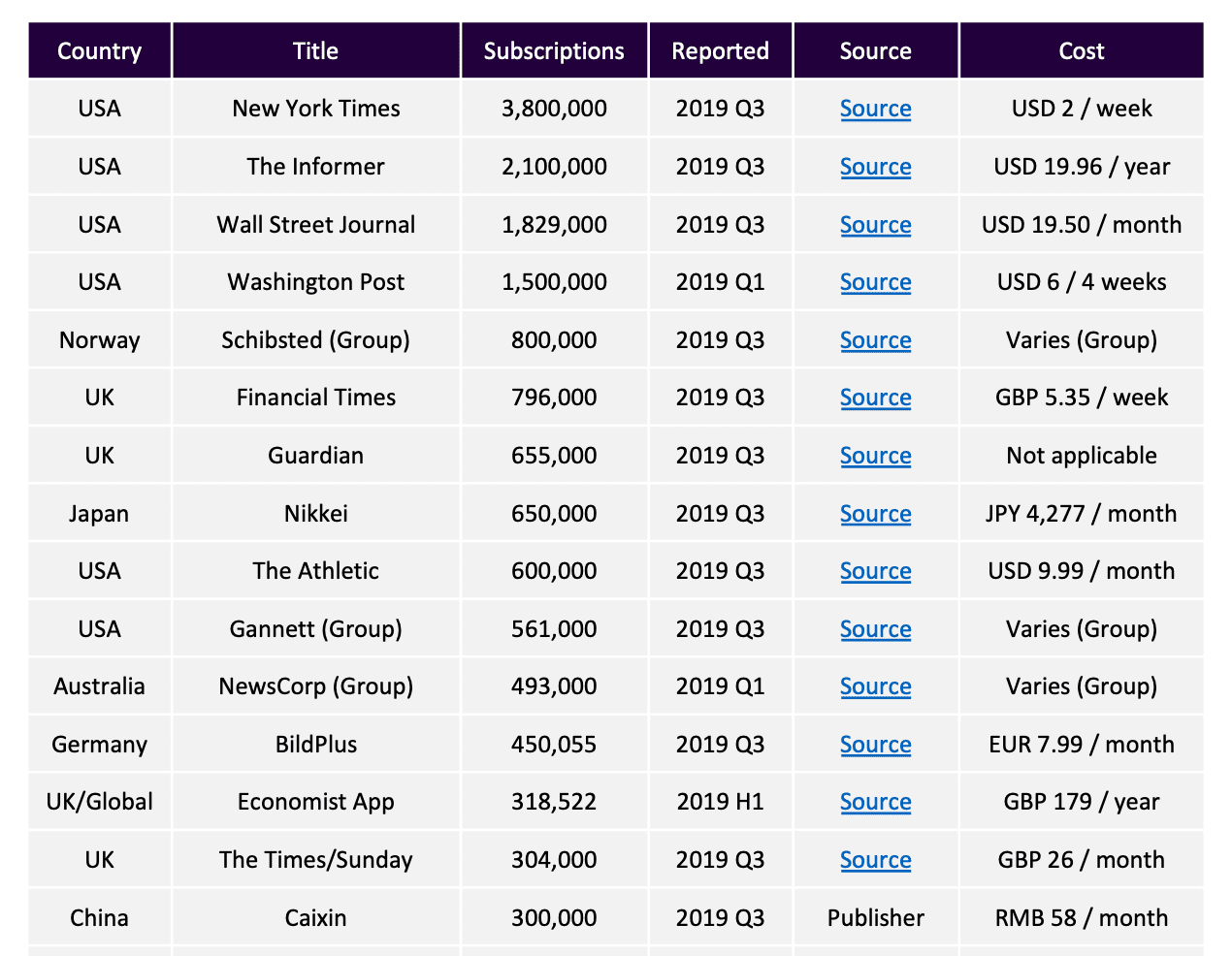

Earnings data from The New York Times Company found that the New York Times now has 5 million subscribers, of whom close to 3.5 million are digital-only customers for their core news product. (The NYT also offers digital subscriptions for Cooking and Crosswords, products which have around 1 million subscribers.)

By 2025, the New York Times aims to have 10 million subscribers, as it continues to pivot towards a subscription-led revenue model. It added 1 million new subscribers in 2019.

In an earnings call, Mark Thompson, President and CEO of the New York Times Company said that this growth of new subscribers represents:

“…The largest number since the launch of the pay model in 2011; indeed, the largest number in the history of The New York Times, and as far as we know, the history of American journalism.”

Earlier in the month The Wall Street Journal revealed that it had hit 2 million digital subscriptions for the first time. This made the Journal, alongside the Times, perhaps, the only other news title to hit this 2 million benchmark.

As Josh Benton points out in Nieman Lab, one other potential contender to join this exclusive club, the Washington Post, is privately owned, “so it’s not obliged to impress Wall Street every three months with boffo numbers… the Post’s digital subscription totals get announced only when it’s useful to the company.” Subsequently, we don’t really know where the Post is at.

In contrast, New Corp’s Dow Jones, a stable which also includes the Barron’s Group, and its Professional Information Business, as well as the Wall Street Journal, were at pains to point out more than just their subscriber numbers, also stressing that “digital accounts for approximately 57% of consumer circulation revenues versus 44% for The New York Times.”

For both companies, digital and subscription revenues are key to their future.

In 2019, the New York Times Company “passed $800 million in annual digital revenue for the first time, an objective it had pledged to meet by the end of 2020. Most of that $800.8 million — more than $420 million — came from news subscribers.”

3: Digital subscriptions doubled globally in 2018-19

Published in June 2018, the first issue of FIPP’s Global Digital Subscription Snapshot identified nearly 10 million digital subscriptions by title. Alongside the New York Times, Wall Street Journal and the Washington Post, their Top 10 also included Bild (Germany) the Financial Times, Economist and Times of London (UK) and Aftonbladet (Sweden).

The report identified that “paid content success requires investment, intelligent application of analytics, an understanding of the local market and leveraging the emotional connection to a brand.” To this, as the journalist Chris Sutcliffe recently observed:

“Driven by competition and an electric political climate, some publications are …. [finding] the strongest sales pitch they can make to subscribers is not by setting out the values they stand for – it’s the values and people they stand against.”

Jump ahead to the end of 2019, and FIPP’s November 2019 update, saw almost double the number of digital subscriptions. Publishers now enjoy more than 20 million digital subscriptions globally.

Commenting on this dramatic growth, James Hewes, President and CEO, FIPP, reflected:

“With Apple expanding its News+ service with a UK rollout in September this year, and Google Subscription Services adding the Subscription Lab and North American Innovation Challenge to its ever-expanding toolkit for publishers, it seems that if anything, the market is set to be redefined as it heads into a new phase of expansion.”

The report highlighted successes from The Athletic (with subscriptions up 600% – although the authors note “its expansion is driven by generous venture capital funding rather than organic growth, making its model challenging to replicate for the average publisher,”) as well as the Dutch title De Correspondent, which expanded its subscription base by 75% with a new English language edition.

To this, “the launch of Apple News+ in the UK during September and the continued expansion of Google Subscription Services suggests that the tech behemoths are smelling potential,” FIPP says.

4: Limits to growth? A bumpy road ahead for some

Despite these impressive headline numbers, FIPP’s analysis also provides some sobering thoughts for publishers.

Although James Hewes pushed back on recent research and commentary which stressed “the potential limitations for the market with terms like subscription fatigue entering the industry lexicon alongside suggestions that the market for news and magazine media digital subscriptions is nearing saturation point.” He nonetheless recognised that “these are valid questions based on solid research.”

One such study, the 2019 Digital News Report, offered a number of insights to support this more cautious worldview.

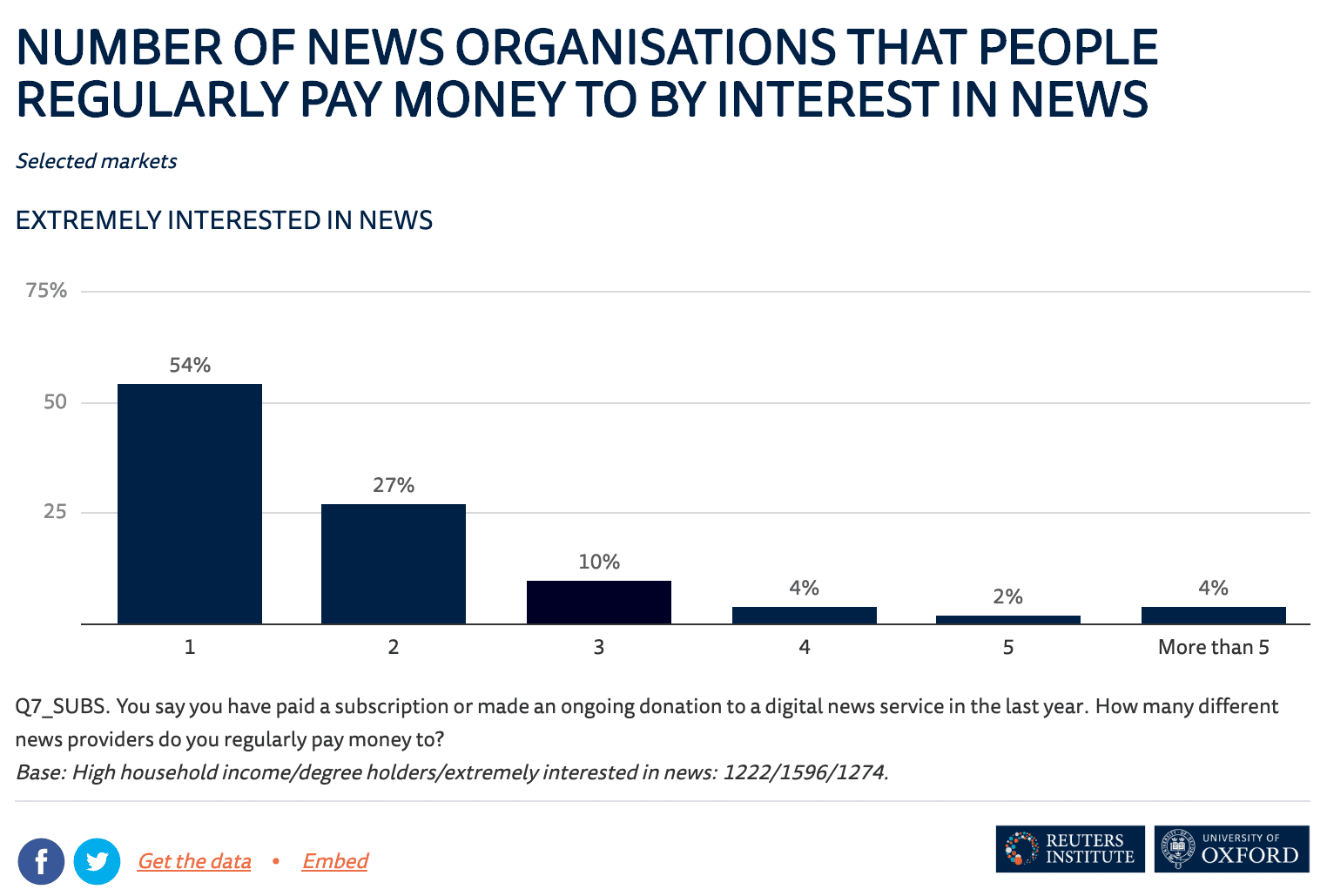

As Richard Fletcher, a Senior Research Fellow at Reuters Institute for the Study of Journalism (RISJ) reminded us, only a minority of news consumers pay for news, and “the average (median) number of news subscriptions per person among those that pay is one in almost every country.”

“But perhaps more importantly, the average almost never exceeds one, regardless of what group you look at. Even among those who are most interested in news, the wealthiest, or the most educated, most people only pay money to one news organisation.

This point matters because, depending on the way subscriptions are distributed among different publishers, it may mean that only a small handful of those that are currently available will be able to attract enough paying subscribers to survive.”

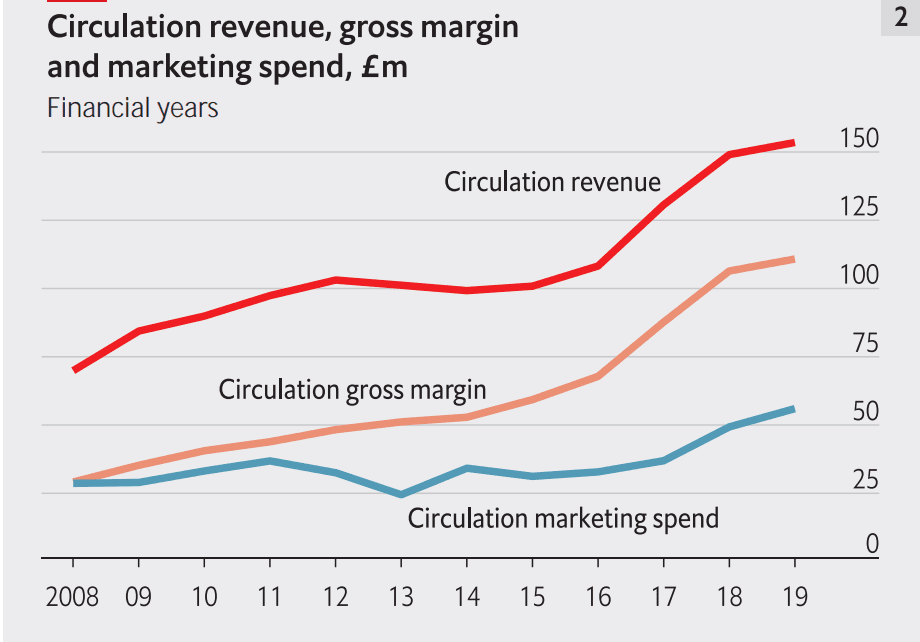

5: Gaining subscribers can be expensive

As we shared in March last year, The Economist – which has seen some success in growing its subscribers base – spent £50m ($65.2m) on marketing in 2018.

The impact of this, Chairman Rupert Pennant-Rea wrote, in The Economist Group’s 2018 Annual Report, is that new subscribers were up by 18%. “But,” he cautioned, “as some existing subscribers also leave each year, it is the net increase that really matters. This was 36,000 last year, to a total of just over 1.1m full-price subscribers.”

That slowed in 2019. New Chairman Paul Deighton wrote that:

“At The Economist, for the third year running, we made another marked increase in marketing investment, spending £56.4m, 14% more than the previous year. Subscriber numbers finished 13,000 higher, at 1,123,000.

This is less than we had hoped, although revenue per copy increased to £2.48, compared with £2.39 last year.”

“The financial results reflect a mixed year,” CEO Chris Stibbs admitted. “There was some growth in revenue, and profits from continuing operations, although robust, declined in line with expectations. The main reason for this decline was the increased spend behind the circulation of The Economist, which continued to reinforce the brand globally but this year did not deliver the expected growth in subscribers.”

What this means for you: three main takeaways

With The Economist spending “almost £7m more in marketing last year than the previous year,” their subscriber numbers show the challenge of converting brand awareness (and consumption on other channels such as social) into direct reader revenues. Marketing spent is no guarantee of conversion. And success can clearly vary year-on-year.

FIPP’s data suggests a similar challenge with projecting on-going performance, given the reshuffled order of publishers in their 2019 rankings.

Their reporting suggests that some publishers will continue to see a continued growth in digital subscriber numbers, driven by factors such as geographic expansion (De Correspondent and The Athletic), new tools for publishers (from Google, Apple et al.) as well as the value that some audiences play on specialist and quality reporting (NYT, WSJ etc).

Nonetheless, as the Reuters Institute’s work implies, there are potential limits to the willingness of audiences to pay for news and the number of outlets they are willing to pay for.

Niche and specialist publications, as well as those with a marquee brand and a large base of potential subscribers to tap into, may well be best placed to ride the subscription storm.

But smaller publications, those without these resources and advantages (such as local news outlets,) may find these waters much harder to navigate.

In my next article, the second and final part of this series, I’ll explore the key strategic implications of the shift to subscription and what this means for publishers.